Efficient Frontier

William J. Bernstein

Efficient Frontier

William J. Bernstein

![]()

The 15-Stock Diversification Myth

One of the most dangerous investment chestnuts is the idea that you can successfully diversify your portfolio with a relatively small number of stocks, the magic number usually being about 15. For example, Ben Graham, in The Intelligent Investor, suggests that adequate diversification can be obtained with 10 to 30 names. In a classic piece in Journal of Finance in 1968, Evans and Archer found that portfolios with as few as 10 securities had risk, measured as standard deviation, virtually identical to that of the market. Over the decades, the "15-stock diversification solution" has become enshrined in various texts and monographs, most famously in A Random Walk Down Wall Street:

By the time the portfolio contains close to 20 equal-sized and well-diversified issues, the total risk (standard deviation of returns) of the portfolio is reduced by 70 percent. Further increase in the number of holdings does not produce any significant further risk reduction.

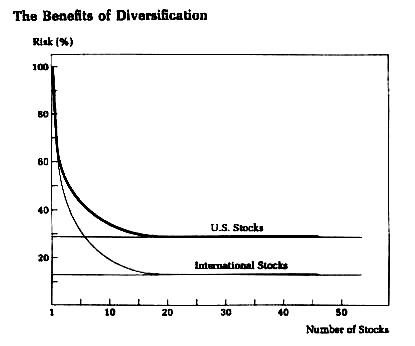

To emphasize the point, Mr. Malkiel collated data from a paper by Bruno Solnik, and combined the reduction in risk of both domestic and international portfolios into one nifty graph:

In a paper recently accepted for publication in Journal of Finance Mr. Malkiel et. al. extend and update the state of our knowledge regarding portfolio diversification and market volatility. It’s a wonderful piece, well-written and quite understandable, and comes to four fascinating conclusions:

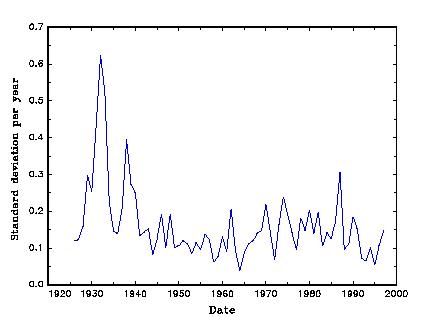

- The volatility of individual stocks has risen over the past few decades (the upper plot represents monthly returns, the lower plot annualized monthly returns):

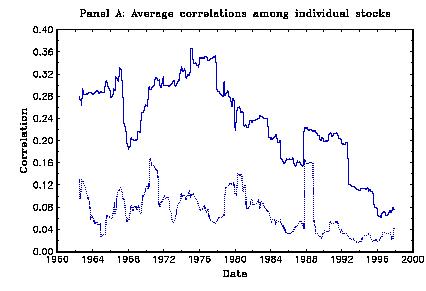

- The correlation among stock returns is falling (the solid upper line represents monthly data, the lower line daily data):

- The effects of #1 and #2 cancel each other out. Consequently, the overall volatility of the market has not changed:

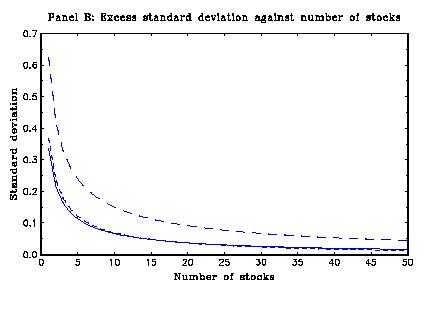

- However, also because of #1 and #2 the number of stocks necessary to eliminate nonsystematic risk is rising (the upper curve represents the more recent period):

This is all profound and important stuff. And, unfortunately, highly misleading. To be blunt, if you think that you can do an adequate job of minimizing portfolio risk with 15 or 30 stocks, then you are imperiling your financial future and the future of those who depend on you. The reason is simple: There are critically important dimensions of portfolio risk beyond standard deviation. The most important is so-called Terminal Wealth Dispersion (TWD). In other words, it is quite possible (in fact, as we shall soon see, quite easy) to put together a 15-stock or 30-stock portfolio with a very low SD, but whose lousy returns will put you in the poorhouse.

This issue has not been much investigated or discussed. One of the pioneers in this area is Edward O’Neal of Auburn, who in a piece in Financial Analysts Journal a few years back looked at TWD as a function of the number of mutual funds. His data show that the risk of TWD falls off as 1/sqrt(n); in other words, a portfolio of four mutual funds is half as risky as one. However, I’m not aware of any definitive studies of TWD as a function of the number of stocks.

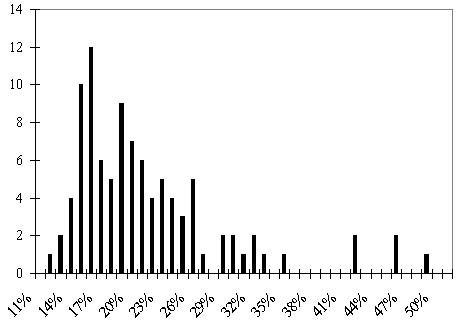

In order to investigate this problem, I looked at the stocks constituting the S&P 500 as of 11/30/99, and formed 98 random equally-weighted 15-stock portfolios for the 12/89-11/99 10-year holding period. Below is a histogram of the annualized portfolio returns:

The "market return" (all 500 stocks held in equal proportion) was 24.15%. This is considerably higher than the 18.94% return of the actual S&P for two reasons: First, the S&P is a cap-weighted, not an equal-weighted, portfolio. Second, and much more important, many of the stocks in the S&P on 11/30/99 were not in the index at the beginning of the period. The recently-added stocks obviously had much higher returns than the companies they replaced, upwardly biasing the entire series of returns. Nonetheless, these flaws in the methodology do not change the basic conclusion; the TWD of these 15-stock portfolios is staggering—three-quarters of them failed to beat "the market." (Had the study been done with the S&P stocks extant on 12/1/99, it seems certain that the positive kurtoskewness of the present sample would have been replaced with a significant negative kurtoskewness—a much more important descriptor of risk. If anybody wants to give me a survivorship-bias-free S&P database for the past 10 years, my modem and mailbox are in fine working order.) Even so, the scatter of returns was quite high, with more than a few portfolios underperforming "the market" by 5%-10% per annum.

The reason is simple: a grossly disproportionate fraction of the total return came from a very few "superstocks" like Dell Computer, which increased in value over 550 times. If you didn’t have one of the half-dozen or so of these in your portfolio, then you badly lagged the market. (The odds of owing one of the 10 superstocks are approximately one in six.) Of course, by owning only 15 stocks you also increase your chances of becoming fabulously rich. But unfortunately, in investing, it is all too often true that the same things that maximize your chances of getting rich also maximize your chances of getting poor.

If the O’Neal data are generalizable to stocks, and I believe that they are, then even 100 stocks are not nearly enough to eliminate this very important source of financial risk.

So, yes, Virginia, you can eliminate nonsytematic portfolio risk, as defined by Modern Portfolio Theory, with a relatively few stocks. It’s just that nonsystematic risk is only a small part of the puzzle. Fifteen stocks is not enough. Thirty is not enough. Even 200 is not enough. The only way to truly minimize the risks of stock ownership is by owning the whole market.

Copyright © 2000, William J. Bernstein. All rights reserved.